There's an aspect of fundraising that rarely gets discussed: density of meetings.

Most founders understand they need to talk to many investors. That part is obvious. But what often goes unmentioned is when those conversations happen and how compressing them into a short window can completely change the dynamics of your raise.

After going through 100+ pitch meetings and raising from VCs in Europe and Silicon Valley, I've seen this play out repeatedly. The founders who spread their investor conversations across months, slowly working through their list one by one, consistently struggle. The ones who stack meetings into concentrated bursts create leverage that transforms the entire process.

To understand why timing matters so much, you first need to understand how investors think and the brutal math working against you.

Let's start with the harsh truth. According to Forbes, only about 1% of startups ever receive venture capital funding. And of those that do raise a seed round, the path forward doesn't get easier.

The funnel below is a resource shared by Henri Pierre-Jacques’ (Co-Founder at Harlem Capital) of a year in review of their fund.

These numbers aren't meant to discourage you. They're meant to help you understand why investors behave the way they do.

To understand why density of meetings with investors matter for you as a founder, you first need to understand how VCs think about their portfolio.

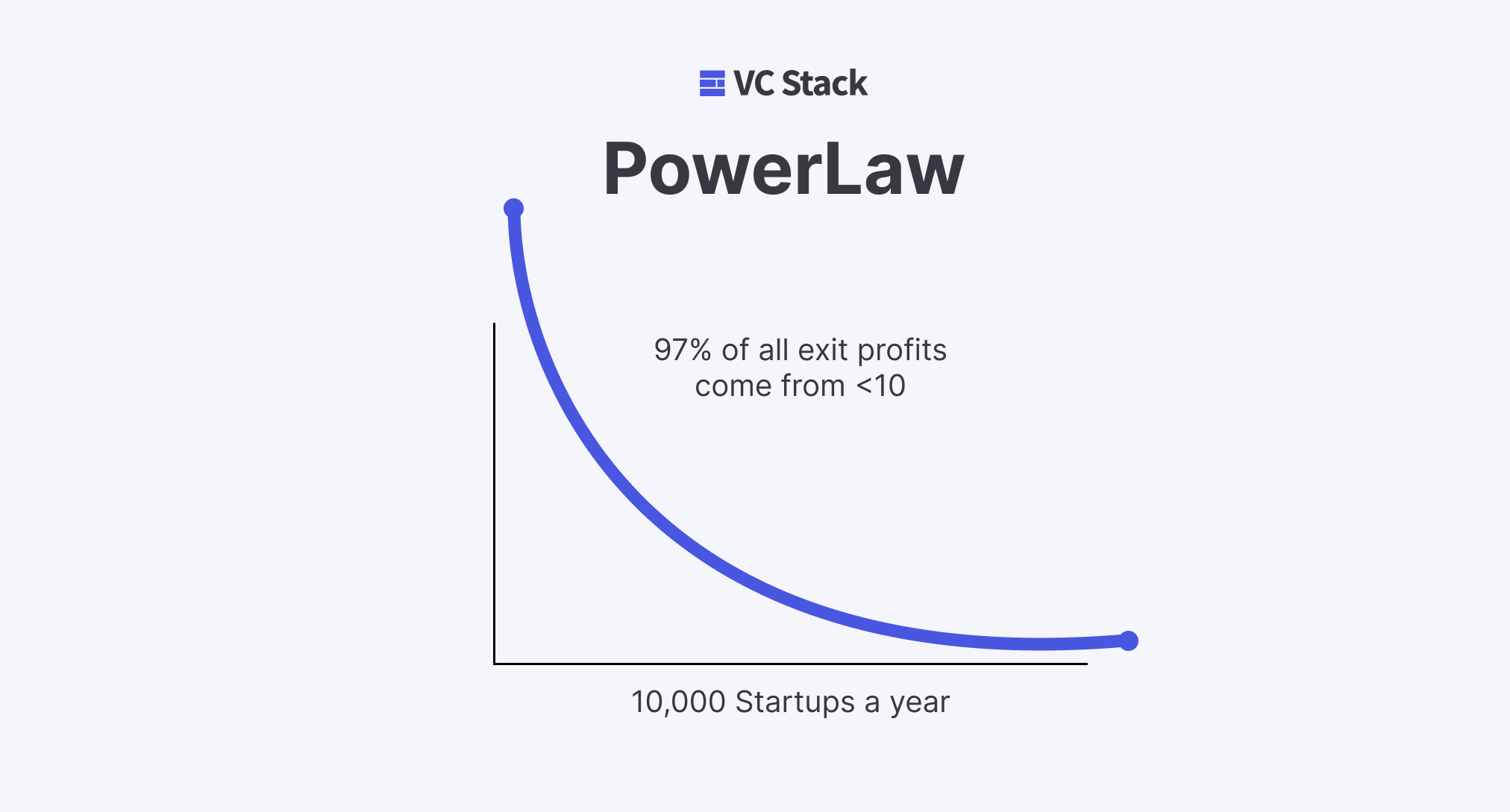

This is The Power Law, the fundamental principle that governs venture capital. Out of 10,000 VC-backed startups, 97% of all exit profits come from fewer than 10 companies.

In a typical scenario, out of 100 startups a standard investor backs, only 2-4 will bring returns that multiply the entire fund. The outcome of the remaining 97 investments essentially becomes irrelevant compared to the overwhelming impact of those few outliers.

What does this mean for you as a founder?

Your mission is to craft a narrative that convinces investors your company could be one of those rare success stories that can return their entire fund many times over.

But here's the catch: investors can't know for certain which companies will be the winners. The data doesn't exist yet. So they rely on something else entirely, and that’s the founding team and their execution.

Not showing signals of demand and interest from other investors shows 2 things, the company is not “hot” for other investors, and the CEO’s execution skills are lacking (at least in fundraising). For investors, this is one of the first filters they use.

VCs are drowning in deal flow. A typical partner at a reputable fund might see hundreds of companies per month but can only invest in a handful per year. This creates an impossible math problem.

Because they can't deeply analyze every company, investors make quick investment decisions based on strong but simple signals:

When an investor gets a cold email, they think: "Why should I prioritize this over the 50 other decks in my inbox?"

When an investor gets a warm intro from a portfolio founder with a note saying "You need to meet this team, I think they're onto something big," the mental calculation changes.

And when that same investor hears that other VCs are looking at the deal*,* you have their full attention.

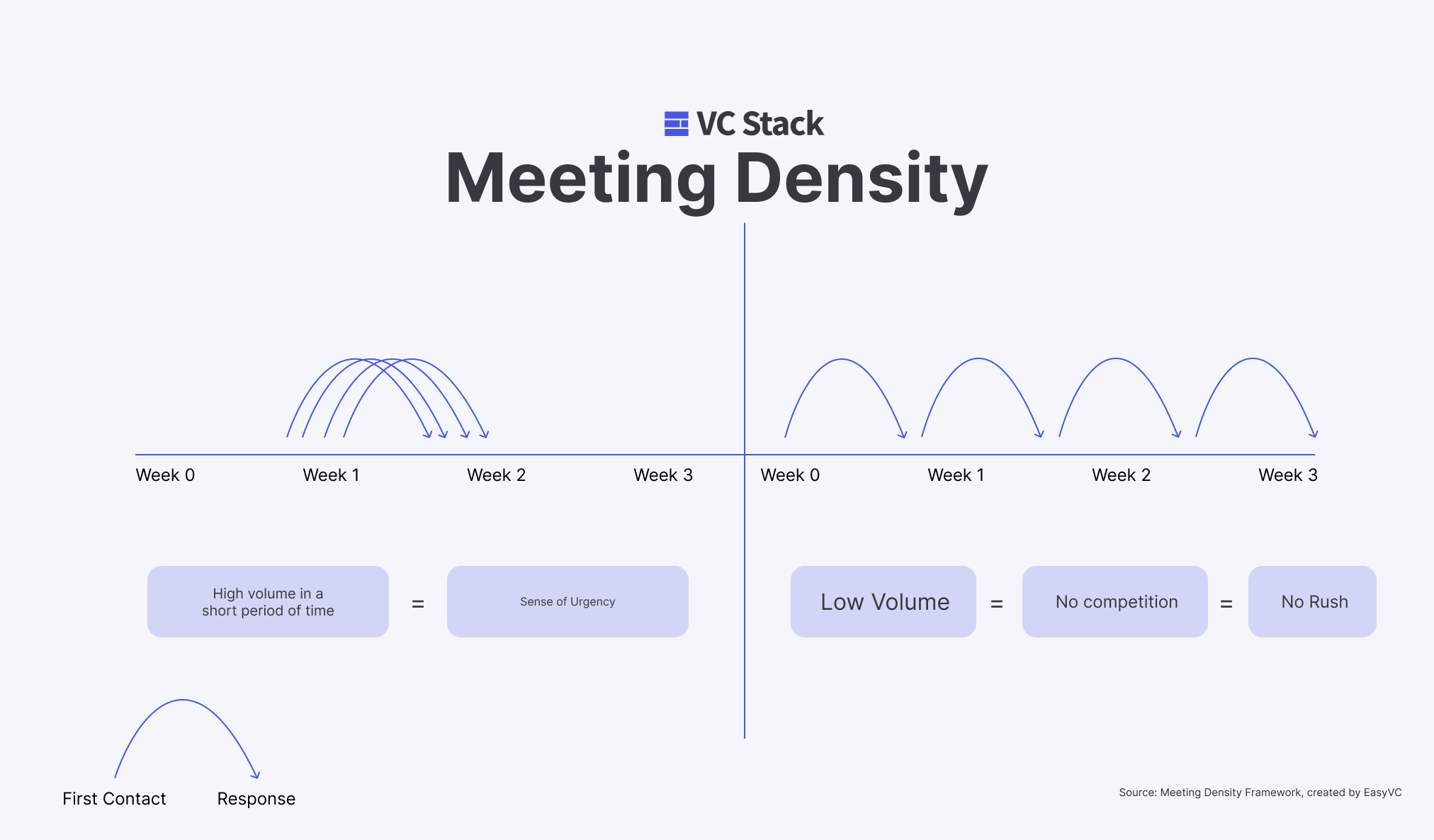

This is where density becomes your most powerful weapon.

The difference between a successful fundraise and a failed one often comes down to timing and concentration.

Left side: High volume in a short period of time = Sense of urgency = Leverage

When you pack multiple investor meetings into a 2-3 week window, several things happen:

Right side: Low volume = No competition = No rush

When you spread meetings over months, investors have no urgency. They think: "Why invest now? I can wait 6 months and see if the founder solves X."

This is exactly what happens when investors tell you "You're too early." They're often not saying your company isn't ready. They're saying they don't feel pressure to decide now.

Creating density requires volume. Volume requires access. But what if you don't have a network?

When I started my company in Spain, I had no Stanford alumni circle, no investor "besties," and no connections in the startup ecosystem. Still, I ended up raising from VCs and living in San Francisco.

The secret? I stopped DM'ing investors directly and started DM'ing their portfolio founders instead.

Here's the process:

In my experience, out of 15 portfolio founders I reached out to:

That was the unlock.

As Marc Andreessen says: "The argument in favor of the warm intro is that it's the first test of your ability to basically network your way to the investor." If you can't get an intro with a VC, how are you going to close massive deals or bring key people onboard?

https://www.youtube.com/watch?v=Pgw0dmftGi8

For each VC on your list, you need to:

Multiply this by 50-100 target investors, and you're looking at weeks of manual work before you even start having investor conversations.

With EasyVC, you can automate the entire warm intro process. The platform:

The founders who consistently raise aren't necessarily building better companies than everyone else. They're often just running a better process.

Fundraising is 50% about how strong your company is, and 50% about how well you run the process.

If you run it right, urgency beats traction in most cases. This is why rounds with seemingly no traction that make you think "How did they raise that much money?" happen.

The math is simple:

Don't spread your fundraise over 6 months with scattered conversations. Build your pipeline, stack your intros, and execute in a concentrated burst.

That's how you turn the odds in your favor.

Special thanks to Daniel Olmedo from EasyVC for guest writing this article.